Economic Growth and Investment

May 14, 2021

Through the challenges of the pandemic to individuals, communities and businesses around the world, we have found reason to be encouraged and optimistic about the future.

The current and next generation of entrepreneurs around the globe are building networks of transformative organizations, changing perceptions of innovation, societal progress and fundamentally, the growth of intrinsic value.

As pioneers of growth equity, General Atlantic has a long history – spanning more than 40 years – of empowering companies to reach new levels of growth and scale to tackle global challenges. The new generations of entrepreneurs each bring a dynamic growth mindset and innovative opportunities to their communities, which spur economic and societal growth. We are proud to partner with them.

Our latest paper from Nobel Laureate and General Atlantic Senior Advisor Dr. Michael Spence explores the drivers behind the shift to inclusive global growth. Dr. Spence addresses the macroeconomic impact of the pandemic, the sectors likely to experience significant growth in the coming decade as a result, and the impact on global entrepreneurship.

With the release of this piece, we are proud to be formally launching the General Atlantic Global Growth Institute. Through this platform, we will seek to advance conversations around what we believe to be the critical drivers of global growth today: innovation, entrepreneurial dynamism and societal contribution to both local and global communities.

Led by Dr. Spence and with forthcoming contributions from thought leaders across our firm’s network, the GA Global Growth Institute will also examine the dynamic between our own work in supporting entrepreneurs in scaling businesses, and broader societal impacts, including digital enablement, financial inclusion, access to healthcare and education, and sustainability.

We believe that to explore the factors impacting global growth, we must take a microeconomic, bottom-up approach. By uncovering technological, sectoral, and entrepreneurial drivers of growth patterns, we can develop a multidimensional perspective that enables us to identify the most exciting opportunities in the digital and global economy.

In today’s environment and through the next critical phase of recovery, we see General Atlantic and our entrepreneurs as key stakeholders in defending, driving and accelerating global growth and the connectivity and progress that comes with it.

We look forward to continued dialogue around these topics in the months and years ahead.

William E. Ford

Chairman and Chief Executive Officer

General Atlantic

This whitepaper has been written solely by Dr. A. Michael Spence. References to “we”, “us,” and “our” refer to Dr. A. Michael Spence and not of General Atlantic (“GA”). This document is not research and should not be treated as research. The views expressed reflect the current opinions and views of Dr. Spence as of the date hereof and neither Dr. Spence nor GA undertakes to advise you of any changes in the views expressed herein. Opinions or statements regarding macroeconomic or financial market trends are based on current conditions and are subject to change without notice.

GROWTH AREAS IN THE POST-PANDEMIC GLOBAL ECONOMY

While overall macroeconomic growth may lag in the post recovery period, there are sectors, technologies and geographies in which outsized growth can be expected. At the broadest level, at least three sectoral categories that seem poised for an extended period of very high growth and innovation are:

- The development, application and expansion of digital technologies,

- Healthcare and biomedical science, and

- The green revolution – meaning reducing the carbon intensity of the global economy much faster than global growth, via increased energy efficiency and reducing the carbon intensity of the energy mix.

Digital Transformations

DIGITAL – A FOUNDATIONAL THEME FOR GA

The experience of the past year has reinforced our long-held belief in a digital future, driven by the many benefits delivered by technology. Across the globe, businesses harnessed technology to overcome the mobility and proximity challenges of prolonged stay-at-home orders and social restrictions, accelerating digital adoption and sparking ideas for further innovation. Multiple sectors have seen years of progress in terms of reach and penetration compressed into a matter of months, with both accelerated innovation and adoption leading to permanent shifts in business and consumer behavior.

Software is enhancing productivity for knowledge workers; the velocity and quantum of consumer spending online continues to surge, with significant growth runways remaining in both emerging and developed markets; and increased consumption of digitally delivered content and social media engagement is being augmented by AI-powered personalization. Digital transformation of business processes and workflows have led to greater operational efficiency, enabling real-time matching of supply and demand, with radically expanded consumer choice. GA sees significant potential in the continued rise of online grocery platforms, B2B marketplaces, digital education and healthcare, the use of IOT across smart city development and recycling-focused technologies.

Digital alternatives have already delivered tangible benefits in driving inclusive growth, particularly among geographically remote populations, in segments including consumer personal finance and fintech. As we look to the future and life “post-Covid,” GA remains focused on harnessing the secular trends changing industries and delivering solutions globally. Our technology expertise extends across all sectors and regions and will enable us to capitalize on these significant opportunities that underpin global growth.

The digital transformation of economies was well underway prior to the pandemic. It accelerated dramatically, especially in terms of adoption, during the pandemic, because it enabled the continuation of business, economic, and other essential activities that would have otherwise been stopped or conducted with unacceptably high health risks.

Post-pandemic, one can expect a partial shift back or reversion. Schools will return to in- person instruction, offices will likely reopen with hybrid models of work location, patients will visit doctors, people will go shopping and travel for business and leisure will return, but not in a mean reverting fashion. Telemedicine will stay and expand as a complement to traditional service models because it is more efficient for certain purposes and it expands the client base that can be effectively served. Schools will deepen the use of technology to enhance the traditional modes of teaching and learning.

Under the pressure of dealing with the pandemic, two things happened. Entrepreneurs and businesses developed innovative solutions to mobility and proximity challenges, many of which proved valuable, and importantly, they developed ideas for further innovation in digital. Users and acquirers of digital technology conducted experiments that would have occurred more slowly and will retain the ones that have durable value. Both accelerated innovation and adoption will lead to permanent change. The expansions in e-commerce, payments, and digitally enabled financial services are permanent. Traditional retail will undergo a process of digital integration of offline and online channels, the so-called omni-channel trend, but turbocharged by a new appreciation for the role of a digital footprint in enhancing resilience.

One clear learning amplified by the pandemic experience is that digital technologies, especially open platform-centered ecosystems, are powerful tools for expanding service delivery to portions of the population where access has been a challenge. Geographically remote populations frequently suffer diminished service and service quality accessibility issues in areas like primary healthcare, education, and access to markets. Digital alternatives create clear benefits in terms of the inclusiveness of growth patterns. Less understood but a high potential is the use of data and algorithms to close informational gaps and expand accessibility for services like credit. Experience in China, where eCommerce and mobile payments are highly penetrated, suggests that large pools of eCommerce and payments data can be used to accurately assess credit quality and risk for large groups of individuals and small businesses whose access to traditional banking channels is limited.

Much of the discussion, especially in developed countries, focuses on automation and its implications for employment. Automation in the pre-AI era has reduced routine jobs, many of them middle class, in all developed economies. AI significantly expands the range of tasks that machines can perform, so we can expect a continuation of this trend in white- and blue-collar employment. Digital technologies tend to have high fixed/development and low-to-negligible variable or marginal costs. That means they become more efficient and competitive the larger the scale of application.

From a social standpoint, the challenge is to transition the skills of a workforce to those that have value working with and around digital powered machines, so that automation becomes intelligent augmentation. This skills transition is not easy and it takes time. Digitally-enabled learning algorithms probably have considerable potential to accelerate this process in a cost-effective way. I would expect this to be yet another growth area in the digital education/training space.

In the digital economy, the entry barriers tend to be low. One doesn’t need a lot of capital in the initial stages, nor a large organization to provide supporting infrastructure. Ideas are tested in the marketplace and among investors. Good ideas can flourish. This is surely part of the explanation of the surge in entrepreneurship globally.

There are some major challenges in realizing the full potential of the ongoing digital revolution. Arguably the most important challenges have to do with data use and potential misuse, especially personal data and its security, use and potential misuse. Norms, laws, rights, disclosure, rules and regulations and best practices surrounding data, their security, and their appropriate use, are crucial enablers of digital transformation, and they are in development. But that process is far from complete. Building trust is emerging as a key element in enabling data driven use cases.

There is an interesting new paper about data by the Luohan Academy, “Understanding Big Data: Data Calculus in the Digital Era.” It addresses the characteristics of digital data, the origins of its value in use, and then addresses the issues related to the responsible and properly regulated uses of data.

Data has to be shared and pooled to create value. It may seem obvious that digital data that are inaccessible, or locked up in data silos, are of little value. But it seems to have somewhat gotten lost in the privacy discussion. It is as if policy makers sense that people seem to want the benefits of accessible digital data and machine learning applications (properly controlled and used) without acknowledging that to achieve them, they first have to be pooled, securely stored and then analyzed. Trust appears to be more important than detailed specifications and opt-in systems in reassuring users about the uses of their data.

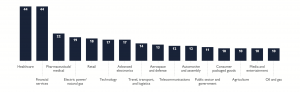

The Luohan Academy paper deals with this. There is also a McKinsey report that deals sensibly with the subject. A graph from the McKinsey report provides an interesting picture of trust across sectors on data:

Consumers view healthcare and Financial-services businesses as the most trustworthy

Respondents choosing a particular industry as most trusted in protecting of privacy and data, % (n = 1,000)

Evolving policies around data privacy and security are sometimes viewed as risk factors. And it is surely a complex area. My view is that done properly, good and well-regulated data management is a key enabler for achieving the potential benefits of digital technology applications. A collaborative approach involving government and business tech sectors will help advance the state of the art in this area.

Biomedical Science, Drugs and Healthcare

HEALTHCARE AND BIOMEDICAL TECHNOLOGIES – AN INFLECTION POINT

The powerful combination of digital technologies and major advances in the application of biomedical sciences is transforming healthcare systems around the world. Across both healthcare and biomedical segments, GA is partnering with visionary entrepreneurs developing crucial, next-generation therapeutic solutions that address the areas of greatest unmet medical need, as well as the life science technologies, tools, and services that support the delivery these therapeutics.

Underscoring GA’s long-term commitment to life sciences, we have formalized it as our fifth core investment pillar. We are uniquely positioned to leverage our global reach, long-term collaborations and deep expertise in both technology and healthcare to capture – and drive – the momentum galvanized by the rapid sequencing of the COVID-19 virus and the development of vaccines across the world. This is a once in a generation opportunity to meaningfully contribute to the evolution of medical provision globally, delivering major innovations in science, the treatment of diseases and disorders, and primary care.

There are many good reasons for thinking we are in the early stages of a “golden age” of biomedical science, not only in the science itself (much of which dates back to the discovery of the structure of DNA) but in applications to medicine, drugs, vaccines, therapeutics, the genetic vulnerabilities to various diseases and disorders, and gene editing. Broadly available, powerful and relatively inexpensive tools have accelerated the rate of progress. Artificial Intelligence in its modern form is one of those powerful tools. The astonishing speed with which the structure of the COVID-19 virus was determined, and effective vaccines developed, is surely an attention-getting example.

Progress in biomedical science and its applications in medicine and healthcare has been turbo-charged by the convergence of digital technology and specifically AI, with the biological and medical science. Large digital databases are accessible and algorithms are being used to study the binding characteristics of molecules in the context the understanding of diseases and the search for drugs. AI is also being deployed to learn about genetic proclivities with respect to a wide range of diseases and health conditions.

We noted above that tele-medicine or tele-health, perhaps better termed internet-based medical and healthcare, expanded rapidly because of the virus and is seen as having the potential to increase the quality and coverage of primary care globally. Home-based diagnostic innovations will further augment the potential and scope of remote medical care as a complement to in-office or hospital-based service delivery. Home diagnostics is already happening and will likely advance rapidly. Regular blood glucose monitoring for diabetics is routinely done at home. The Series 6 Apple Watch monitors blood oxygen levels and recent watch series also have an EKG capability. Image recognition algorithms are beginning to be used to detect potential skin cancers and diabetic retinopathy. One can think of these things as preliminary screens or tests that, depending on the outputs, can trigger and motivate in-person visits to medical care facilities, followed by early detection and this is just the beginning.

Healthcare commands a large and growing share of most developed economies. In some cases, like the U.S., the sector accounted for roughly 18% of GDP, prior to the pandemic.1 It is growing in most economies in part because of aging. Some of the investment opportunities may be targeted at efficiency and, hence, shifting the trajectory of costs. That would be a major added side benefit and a growth area. Thus, we have the prospect of major innovations in science, the treatment of diseases and disorders, primary care delivery and efficiency and cost. Geographically, the innovations and growth companies look set to come from a wide range of countries that have the human capital and the requisite public sector commitment to investing in science.

The structure of the healthcare and health insurance systems do matter. In the end, innovative products and services have to find their way to consumers through that system. Structural inefficiencies and misaligned incentives will have an impact on the returns to investment. Healthcare system reform can increase the impact of the flood of innovation that is coming. I just finished reading “The Code Breaker” by Walter Isaacson. We have made stunning progress in gene editing. What is so interesting about this – well, at least one thing – is that scientists figured this out by learning how bacteria do it to defend themselves from viruses.

Last year, the Nobel Prize in Chemistry was awarded to a team that essentially discovered how bacteria identify, “remember” and attack viruses, a key discovery that led to gene editing. It has been described as the most important discovery in biochemistry and biology since the discovery of the structure of DNA. A leading American biochemist who is most well-known for her work in CRISPR gene editing, Jennifer Anne Doudna, is an internationally lauded figure and was awarded this 2020 Nobel Prize in Chemistry, along with Emmanuelle Charpentier.

The Greening of The Growth Model

THE GREEN ECONOMY – CHOICE BECOMES NECESSITY

We are at a pivotal moment in the global economy’s low-carbon transition. Sustainability has become a viable and critical commercial venture and is set to define the next era of corporate existence and value creation. The decarbonisation of the global economy; resource efficiency and conservation; the circular economy; and nature-based solutions now all play a part in corporate accountability.

Concern about climate change and its impact on human health is high on the global agenda and investors must play their part in setting targets and supporting measurable progress towards the decarbonisation of companies, sectors and economies globally.

The pace and scale of disruption will be greater than in any previous industrial transformation, bringing increased scrutiny of values, behavior, and supply chains. Sustainability is no longer a moral preference but a necessity for all economies globally, demanding the collaboration and innovation of investors and entrepreneurs around the world.

The third candidate on my list for extraordinary innovation and high growth is the transformation of the global economy to an environmentally sustainable path, the principal (but not the only) element of which is climate, CO2, and the buildup of the stock of greenhouse gases in the atmosphere. The two main levers available to meet this challenge are energy efficiency and the carbon intensity of the energy mix. Two other key parameters that determine carbon emissions growth are global growth in per capita income (driven mainly by growth in emerging economies) and population growth. Neither of these last two are viewed as the object of climate change mitigation policy, or much alterable. But they matter. Population growth and rising incomes in the developing world makes controlling CO2 emissions even more challenging than it would otherwise be.2

There are several reasons green growth is a likely candidate for an extended period of high growth that stem from policy and from the demand and supply side of the economy.

With the U.S. rejoining the Paris Accords, there is a near universal commitment to tackle the challenge globally. Furthermore, everyone knows that the existing commitments under the Paris agreement are insufficient to solve the problem. Nations and the global community (governments, businesses and society in general) will have to up their game. This will mean, among other things, that an additional commitment of public resources to science and to the development of mitigation technologies. This is exactly the kind of extended public investment that now underpins the biomedical revolution and has provided an upstream foundation for scientific and engineering innovation.

Policies should include incentives for the private sector to develop technologies that increase energy efficiency or that cost-effectively lower the carbon intensity of the energy mix. The business sector will continue to expand their commitment to sustainability under the ESG and multi-stakeholder banners and will be looking for solutions that help deliver on those commitments.

In short, governments are committed, business and finance institutions are engaged and increasingly committed to be part of the solution, and there is a broad and rising sense of urgency in population. In other words, there is a huge demand for solutions. And that is in part what creates the opportunity on the supply side. All these sectors and stakeholders need tools, technologies and business models to deliver on their commitments. Compelling innovations and growth companies should emerge to meet the challenge.

The costs of important green electricity generation technologies, like solar and wind, have come down so quickly that by most accounts are now competitive with fossil fuel technologies in electricity generation. Much of the incremental electric generation capacity and infrastructure that affects energy efficiency globally is still to be built in the coming decades mainly in emerging markets. So, the issue is not replacing systems already in place, but rather building the right ones going forward. In addition, carbon needs a price if market incentives are to be aligned with sustainability objectives. There are now partial carbon pricing systems, and a growing voluntary carbon offset market. It is not unreasonable to expect carbon pricing to expand. That will enhance the returns to low carbon technology investments. In addition, digital technologies are expected to have a central role in the sustainability transformation, via smart grids, energy efficient systems, electrification of the transport sector and more.

Robert Zoellick wrote a very interesting book, “America in the World: A History of U.S. Diplomacy and Foreign Policy.” Among its many insights is that U.S. policy, which varies considerably over our history, at its best is both strategic and pragmatic, and is always constrained by domestic politics. It is an apt framework for understanding the current situation. With the changing of the President, U.S. foreign policy, including policy with respect to China, will become more considered and strategic, and probably more predictable than it was under the Trump administration, but it is severely constrained by domestic politics and domestic challenges.

A short version of what we might expect is as follows. Policy bandwidth in the U.S. will be stretched and will largely be focused domestically on the pandemic, on economic recovery, and on arresting trends in inequality. The Biden administration is not, like its predecessor, anti-multilateralism. It will return to a multilateral framework. Immediate steps already taken were the U.S. rejoining the Paris Climate Accords and the World Health Organization (WHO), an agency of the United Nations. Longer term, the Biden administration has made it clear that it will have a serious climate/sustainability agenda.

With respect to China, any policy stance has to take into account domestic attitudes. In the U.S., among elected officials and certain subsets of the public, sits some bipartisan disagreement with China’s current leadership, based on many things including differences in governance, values in areas like free speech, barriers to market access for digital technology companies, unfair practices like “forced” technology transfer, regional aggressiveness in east Asia, and, of course, human rights. Whatever administration insiders might think about the relative merits of these various areas of tension, at this point they cannot afford to use up political capital by appearing to “go soft” on China, at this point.

Therefore, it seems reasonable and fairly safe to assume that in the short run, this administration will maintain an outwardly aggressive posture with respect to China, while changing relatively little. The incoming Secretary of the Treasury, who is not normally noted for her aggressive approach to communication or policy, was quite harsh on China in her confirmation hearing, affirming statements by a Republican Senator that China has engaged in unfair competition, forced technology transfer, barriers to market access, possibly currency manipulation and more. By the way, the Secretary of the Treasury is the official who reports annually to Congress on China’s currency manipulation (if any) and chairs the internal government board called CFIUS that reviews foreign investments in the US.

That said, there are fairly obvious areas of mutually beneficial cooperation in climate action, healthcare and medicine, among others. It is not unreasonable to expect some quiet, below the radar initiatives in these areas.

Meanwhile, the new administration is expected to attempt to reestablish cooperative relations with Europe, its neighbors, Canada and Mexico, and probably some key Asia/ Pacific allies. Further down the road when the pandemic is past and a full economic recovery has been achieved, we probably can expect selective movement toward cooperation with China, in areas like climate change, health, nuclear arms, mostly likely in a multilateral rather than bilateral context. Climate change is viewed as sufficiently urgent that immediate cooperation in a multilateral setting is a reasonable expectation. Bilateral negotiations with China on issues of contention involving digital technology and national security are likely to be down the road or very quiet.

Tensions around technology and technology intellectual property will not recede, for both economic and national security reasons. They may be handled in a more predictable and manner in this administration. Digital protectionism motivated by mainly by economic and national security considerations, seems set to be with us for the foreseeable future. For multinational companies, and to a lesser extent an investor operating across borders, and especially in the US and China, it will remain a complex and somewhat risky and unpredictable environment.

Concluding Thoughts

We are living in a period of considerable uncertainty, about the longevity of the pandemic, about markets and valuations, public finances and inflation, international cooperation and potential conflict, and about our collective ability to deal with existential challenges like climate. At this point, one can have reasonably optimistic prospects for an exit from the pandemic (or at least its most severe form). But underneath all this, we are living in a period of rapid multi-dimensional technological and economic transformation that creates both big opportunities for investors, entrepreneurs and society. But alas with all big transformations, there are challenges as well that require the sustained engagement of all sectors including ours.

1 Centers for Medicare & Medicaid Services, National Health Expenditure Accounts, Updated 16 December 2020.

2 A useful way to think about carbon or CO2 emissions is the accounting formula: TOTAL EMISSIONS = (POPULATION) X (PER CAPITA INCOME) X (ENERGY PER UNIT OF GDP) X (CO2 PER UNIT OF ENERGY). If you take the log of both sides of this equation and differentiate with respect to time, you get: GROWTH IN TOTAL EMISSIONS = POPULATION GROWTH + GROWTH IN INCOME PER CAPITAL + GROWTH IN ENERGY PER UNIT OF GDP + GROWTH IN CO2 PER UNIT OF ENERGY.

We want the left side to be negative because we are way over a safe carbon budget now. The first two terms on the right are positive. The second two terms need to be negative and together larger than global economic growth. Global CO2 emissions are currently at about 2.5 times what scientists consider a reasonably safe level. And we don’t have a lot of time, because CO2 is building up in the atmosphere. The carbon intensity of the global economy is the product of its energy efficiency and the carbon intensity of the energy mix. A simple calculation shows that to achieve the safe level target in 25 years, the carbon intensity of the global economy will have to decline at a rate equal to the growth of the global economy plus 3.6% per year. So, to be concrete, if the global economy grows at an average of 3% a year, the carbon intensity has to decline at 6.6% for 25 years.