Reinsurance and the Next Phase of Growth in Life and Annuity Markets

by Lara Devieux, Managing Director and Sean McCorry, Managing Director

The Baby Boom has become the Retirement Boom. In the United States alone, more than four million people will reach age 65 each year through the end of the decade.1 By the mid-2030s, meanwhile, seniors are expected to constitute a larger portion of the country’s population than children. Similar demographic shifts are occurring in other developed markets as Japan and Europe.2

While retirees are living longer than previous generations, their retirement security has not kept pace. According to the Swiss Re Institute, the retirement savings gap, or the shortfall between the amount of money people have saved for retirement and the actual income needed to maintain a desired standard of living, stood at $106 trillion across eight global markets in 2022.

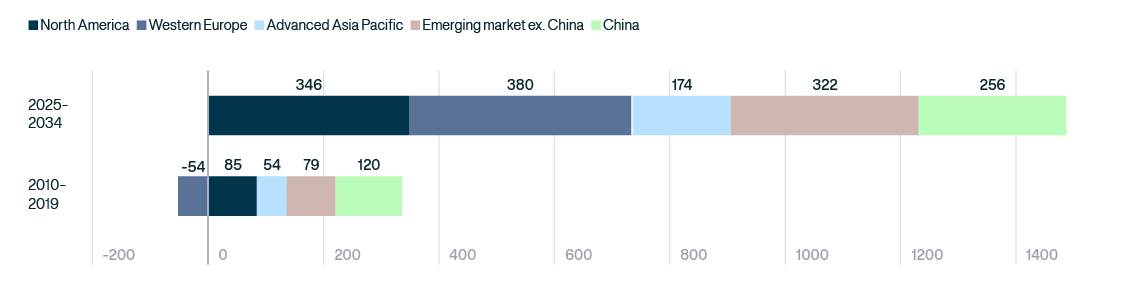

Life and annuity companies are in a position to improve retirement security through product offerings and solutions that provide savings accumulation and guaranteed income over a long horizon. Overall, industry premiums are expected to reach $4 trillion worldwide by 2034, a growth rate five times greater than the increase in premiums seen during the 2010s. Annuity sales in the U.S., meanwhile, reached a record $461 billion in 2025 and are expected to increase as more 401(k)s and other defined benefit plans incorporate annuities into their plan offerings.3,4

To keep up with this demand, life and annuity companies are turning to reinsurance – a risk management tool that functions as insurance for insurance companies. By allowing life and annuity companies to transfer legacy and ongoing liabilities, reinsurers provide the capital needed to expand insurers’ capacity to offer retirement and protection products at a greater scale.

Favorable Long-Term Growth Prospects for Global Life & Annuity Market5

We believe the evolution of the life and annuity ecosystem is creating a compelling investment opportunity in the reinsurance sector. As insurers seek partners that can provide both capital and sophisticated asset management capabilities, a new generation of reinsurance platforms is emerging to meet that demand.

Why Reinsurance Matters

Managing balance sheet growth and capital levels is an increasingly important priority for insurance companies. Working with reinsurers provides support in several ways.

Through reinsurance transactions, insurers transfer blocks of liabilities or flows of new business to specialized partners. These arrangements can provide insurers with capital relief, balance sheet flexibility, and the ability to continue expanding product offerings. In recent years, this activity has accelerated through asset-intensive reinsurance structures, in which reinsurers assume long-duration liabilities backed by investment portfolios designed to generate predictable spread income.

For insurers, these partnerships can unlock additional capacity to originate new business while maintaining strong capital positions. For reinsurers, meanwhile, these liabilities may provide access to stable and recurring sources of income when supported by disciplined asset-liability management and high-quality investment portfolios.

A New Investment Opportunity

Historically, investors seeking exposure to life and annuity markets largely accessed the sector through publicly traded insurance companies. Today, a different entry point is emerging: direct investment in reinsurance platforms.

Many of these platforms are newly-established entities designed specifically to participate in asset-intensive reinsurance markets. Often headquartered in Bermuda due to its attractive and robust regulatory regime, they benefit from an established talent infrastructure and strong risk management frameworks.

We believe these platforms offer investors several valuable characteristics.

First, the economics of life and annuity reinsurance can generate stable spread-based income through the difference between asset yields and liability costs. These earnings may support attractive dividend distributions to investors over time, while also funding the continued growth of the platform.

Second, reinsurance investments tend to have relatively low correlations with traditional asset classes such as public equities and corporate credit, potentially offering investors diversification benefits within institutional portfolios.

Reinsurance Has A Low Correlation to Most Asset Classes6

Finally, as reinsurance platforms scale and diversify their liability portfolios, investors may benefit from long-term value creation alongside current income generation.

The Importance of Platform Quality

While the opportunity in reinsurance is significant, outcomes can vary widely depending on the quality of the platform.

Successful reinsurers typically combine strong liability sourcing capabilities with disciplined underwriting and asset management. Access to a consistent pipeline of liabilities from insurance partners is essential for growth.

Equally important is the ability to manage the assets backing those liabilities. Investment performance, credit discipline, and effective asset-liability management are central to generating stable spread income over time.

Finally, experienced leadership teams and robust governance frameworks are critical to managing risk across underwriting, investment, and operational functions.

Looking Ahead

The structural forces driving growth in life and annuity markets show no signs of slowing. Aging populations, longer lifespans, and evolving retirement systems will likely continue to increase demand for income-oriented financial products that provide predictable income in retirement. Reinsurance plays an increasingly important role in enabling insurers to meet that demand.

For long-term investors, the sector offers exposure to a growing market alongside the potential for stable income generation, attractive dividend distributions, and portfolio diversification.

Download the full white paper here.

For inquiries, please contact Lara Devieux or Sean McCorry.

1 LIMRA (“The US Has Reached The Peak of 65”), April 2024.

2 United Nations, “World Population Prospects 2022/2024”, Accessed March, 2026.

3 LIMRA. “U.S. Retail Annuity Sales Top $460 Billion in 2025, Marking Fourth Year of Record Sales.” February, 2026.

4 LIMRA. “The 2026 Annuity Sales Outlook Remains Strong.” January, 2026.

5 Swiss Re Institute, “Life Insurance In The Higher Interest Rate Era,” May 2024.

6 Source: General Atlantic.Illustrative correlation table as of July 2025. Historical returns start in 2Q2014, the earliest common start date. Public equity returns represented by the S&P 500 Total Return Index. High Yield returns represented by the ICE BofA US High Yield Index. Investment Grade returns represented by Bloomberg US Aggregate Bond Index. Private Equity returns represented by the Bloomberg Buyout Private Equity Index. Private Credit returns represented by the Bloomberg Debt PE Index. Real Assets returns represented by the Bloomberg Real Assets PE Index. Hedge Fund returns represented by the Bloomberg AllHedge Index. Reinsurance returns represented by Return on Equity of the top 5 largest life insurance based on invested assets on a statutory basis (MetLife, NY Life, MassMutual, Northwestern Mutual and TIAA). Due to the lack of availability of a widely published private reinsurance performance benchmark, return on equity is used as a performance proxy for underwriting and investment profitability.

The views expressed in this piece are solely those of the author and are provided for informational purposes only. They should not be construed as investment, financial, legal, or other professional advice. This is an opinion article and does not constitute a recommendation or endorsement of any particular strategy, security, or investment. Readers should conduct their own research and consult with qualified professionals before making any financial decisions. GA does not accept or assume responsibility to you or any other person in connection with the provision of the Information. You acknowledge that you have made, and will continue to make, your own investment decisions without reliance on any representation or warranty of, or advice from, GA or its representatives.

Subscribe and stay up to date with the latest news.